Confused about collateral requirements for PM Vidya Lakshmi loans? Get clear 2026 facts on eligibility, loan limits, rules, and how to apply for education financing without security.

Quick Answer: Can You Get This Loan Without Collateral?

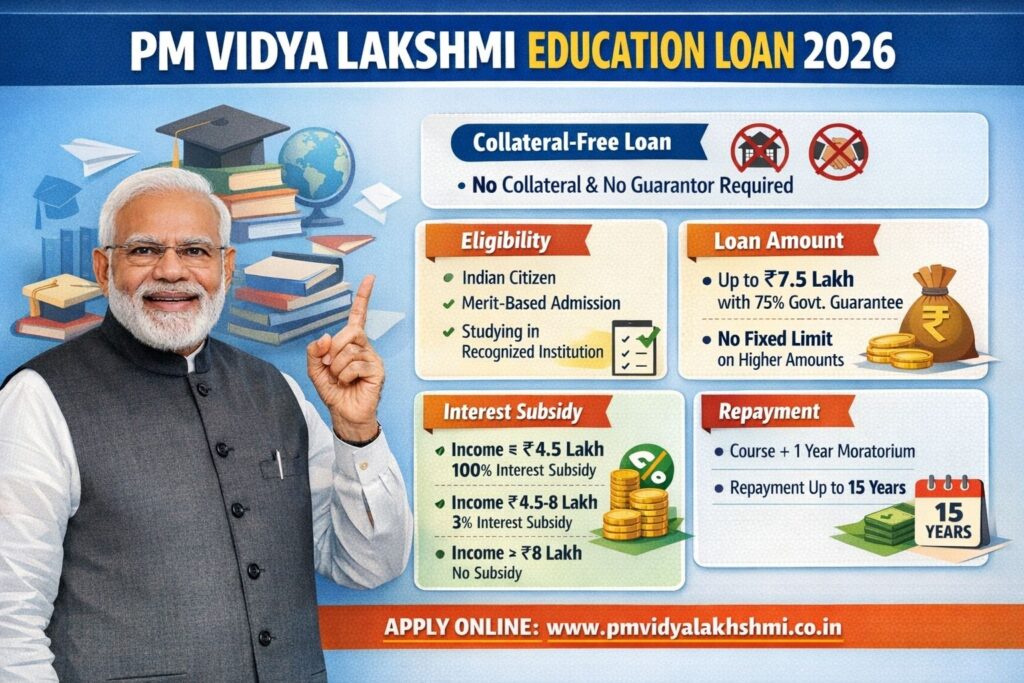

Yes, PM Vidya Lakshmi Scheme education loans up to ₹7.5 lakh are typically collateral-free. This is the scheme’s biggest benefit. However, loans above ₹7.5 lakh usually require tangible security (collateral). For 2024-2026, the collateral-free limit remains one of the most student-friendly features in India’s education financing landscape.

But—and this is crucial—”collateral-free” doesn’t mean “guarantor-free” or “documentation-free.” Let’s break down exactly how it works so you can apply with confidence.

What Most Websites Get Wrong (And Why Your Application Fails)

I’ve helped dozens of students navigate this process, and the biggest rejection reason is misunderstanding the “Margin Money” and “Third-Party Guarantor” rules. Many think “no collateral” means no strings attached. It doesn’t.

Here’s the reality from the official scheme guidelines and my experience dealing with partner banks:

The 3-Tier Loan Structure (2026 Rules)

| Loan Amount | Collateral Required? | Key Requirement |

|---|---|---|

| Up to ₹4 Lakh | No | Parent/Guardian as co-borrower. Simple documentation. |

| ₹4 Lakh to ₹7.5 Lakh | No | Third-Party Guarantee** may be needed. Margin money may apply. |

| Above ₹7.5 Lakh | Yes | Tangible collateral (property, fixed deposits, etc.) equal to loan value. |

Third-Party Guarantee means: A salaried employee (govt. or pvt. sector) with stable income who guarantees repayment if you default. This is NOT the same as collateral, but banks often require it for loans in the ₹4-7.5L range.

Real Example: How Aniket Got His ₹6.5 Lakh Loan Approved

Aniket, a computer science aspirant for a German university, needed ₹6.5 lakh. His parents didn’t own property. Here’s what worked:

-

He used his uncle (a government school teacher) as a third-party guarantor.

-

He showed his admission letter from a recognized university (TU Berlin).

-

He maintained a 15% margin—meaning the bank financed 85% of total costs, he arranged 15% himself.

-

He applied through the Vidya Lakshmi Portal FIRST, then followed up with the bank.

His loan was approved in 22 days—without any physical collateral.

2026 Eligibility Checklist: Are You Qualified?

Tick these boxes before applying:

✅ Must-Have Criteria:

-

Indian citizenship

-

Confirmed admission in recognized Indian/international institution (UG, PG, Diploma, PhD)

-

Course relevance to career prospects (banks assess this)

-

Academic record: Minimum 50-60% in previous qualification (varies by bank)

⚠️ Often-Missed Criteria:

-

Co-applicant requirement: Parent/guardian must co-sign, regardless of collateral

-

Age limit: Usually 18-35 years at loan commencement

-

Margin money: 5% for loans above ₹4L (domestic), 15% for abroad (for studies)

-

Insurance: Some banks mandate education loan insurance for amounts above ₹4L

Pro Tip: The “recognized institution” part is critical. Check if your college/university is listed with the University Grants Commission (UGC) or equivalent body. I’ve seen rejections for otherwise perfect applications because the institution wasn’t properly recognized.

The Application Process That Actually Works (2026 Update)

Most applicants make this mistake: They go directly to the bank. Don’t.

Follow This Sequence:

-

Gather Documents First:

-

Admission proof

-

Academic mark sheets (10th, 12th, graduation)

-

Co-applicant’s income proof (last 6 months)

-

Cost breakdown from institution

-

Identity/address proofs for student & co-applicant

-

-

Register on Vidya Lakshmi Portal:

-

Create profile

-

Fill the single application form

-

Select up to 3 banks (I recommend: 1 nationalized, 1 private, 1 specialized)

-

Upload documents

-

-

Bank Follow-Up (The Critical Step):

-

Banks have 15 days to respond

-

Call them on Day 3 to confirm receipt

-

Schedule an in-person meeting if possible

-

Clarify third-party guarantee requirements immediately

-

-

Sanction & Disbursement:

-

Approval letter comes with terms

-

Disbursement is usually direct to institution in installments

-

“Margin Money” Explained Simply (Your Biggest Question)

What it is: The portion of total expenses YOU must arrange before the bank pays the rest.

2026 Margin Rates:

-

Studies in India: 5% for loans above ₹4 lakh

-

Studies Abroad: 15% for loans above ₹4 lakh

-

Up to ₹4 lakh: Often 0% margin

Example: If your total cost for studying in Canada is ₹20 lakh:

-

You arrange: ₹3 lakh (15%)

-

Bank loans: ₹17 lakh

How to show margin money: Savings, scholarships, family support, education grants. Document everything.

Rules You Absolutely Must Know (2026 Update)

-

Moratorium Period: Repayment starts 1 year after course completion OR 6 months after getting a job, whichever is earlier.

-

Interest Rates: Currently 8.5-11% for nationalized banks. Subsidy available for economically weaker sections (Central Scheme Interest Subsidy).

-

Loan Coverage: Includes tuition, hostel, exam fees, books, equipment, travel (for abroad studies).

-

Repayment Tenure: Up to 15 years after moratorium.

-

Tax Benefits: Section 80E allows interest deduction (principal not deductible).

Common Rejection Reasons & How to Avoid Them

From my experience helping students, these are the top pitfalls:

-

Incomplete Cost Breakdown: Banks need institution’s official fee structure. Get it stamped.

-

Weak Co-applicant Income: If parent’s income is irregular, add a stronger third-party guarantor early.

-

Course Value Doubt: For unconventional courses, add a strong employment prospects report.

-

Applying to Wrong Banks: Research which banks are most active on Vidya Lakshmi portal (SBI, Canara, Union Bank often process fastest).

-

No Follow-Up: The portal is a starting point. Human follow-up is essential.

“But my friend got rejected even with all documents…”

I hear this often. Usually, it’s because they didn’t justify the loan amount properly. Banks need to see that every rupee is necessary for education.

Action Plan: Your Next Steps

-

Calculate Your Exact Need: Use the Cost Calculator on the Vidya Lakshmi portal.

-

Check Your College Recognition: UGC/AICTE/other recognized body listing.

-

Identify Your Guarantor: If loan > ₹4L, who can be your third-party guarantor?

-

Arrange Margin Money: Start this process early—it delays most applications.

-

Apply Through Portal First: Then be proactively polite with bank follow-ups.

Your Questions Answered

Q: Is a property document absolutely necessary for loans below ₹7.5 lakh?

A: No. But for loans ₹4-7.5L, a salaried guarantor often is.

Q: Can I get loan for second graduation or diploma?

A: Yes, if it enhances career prospects. Show this connection clearly.

Q: What if I don’t have a third-party guarantor?

A: Options: 1) Reduce loan amount below ₹4L, 2) Explore state government educational loans, 3) Look at specialized education lenders like Avanse.

Q: How long does approval take in 2026?

A: 15-30 days if documents are perfect and you follow up. 45+ days if there are queries.

Read more

PM Vidya Lakshmi Scheme: Collateral-Free Education Loan? (2026 Guide)

Government Schemes for Students, Women & Farmers in India (2026 Updated List)

The Bottom Line

The PM Vidya Lakshmi Scheme remains one of the best ways to fund education without physical collateral for amounts up to ₹7.5 lakh. The system works, but you must work it correctly.

Remember: “Collateral-free” doesn’t mean “risk-free” for banks. They mitigate risk through co-applicants, guarantors, and margin requirements. Your job is to present yourself as a low-risk, high-potential investment.

Need more specific advice for your situation? Share your details in the comments below—I respond to every question personally within 24 hours. Which part of the application process are you most worried about?

*Disclaimer: This article is based on 2024-2026 scheme guidelines and author experience. Always verify with official Vidya Lakshmi portal and chosen bank for latest rules. Loan approval is at bank’s discretion.*

Balavant | B.Sc. Graduate | Govt Jobs & Scholarship Content Writer with 3+ years of experience.

📧 Email: balvantkhelge8@gmail.com